Creating a monthly budget is one of the simplest ways to take control of your finances. But many people struggle because they don’t know where to start or what categories to include. If you’re completely new to budgeting, start with our Beginner’s Guide to Budgeting before using a template.

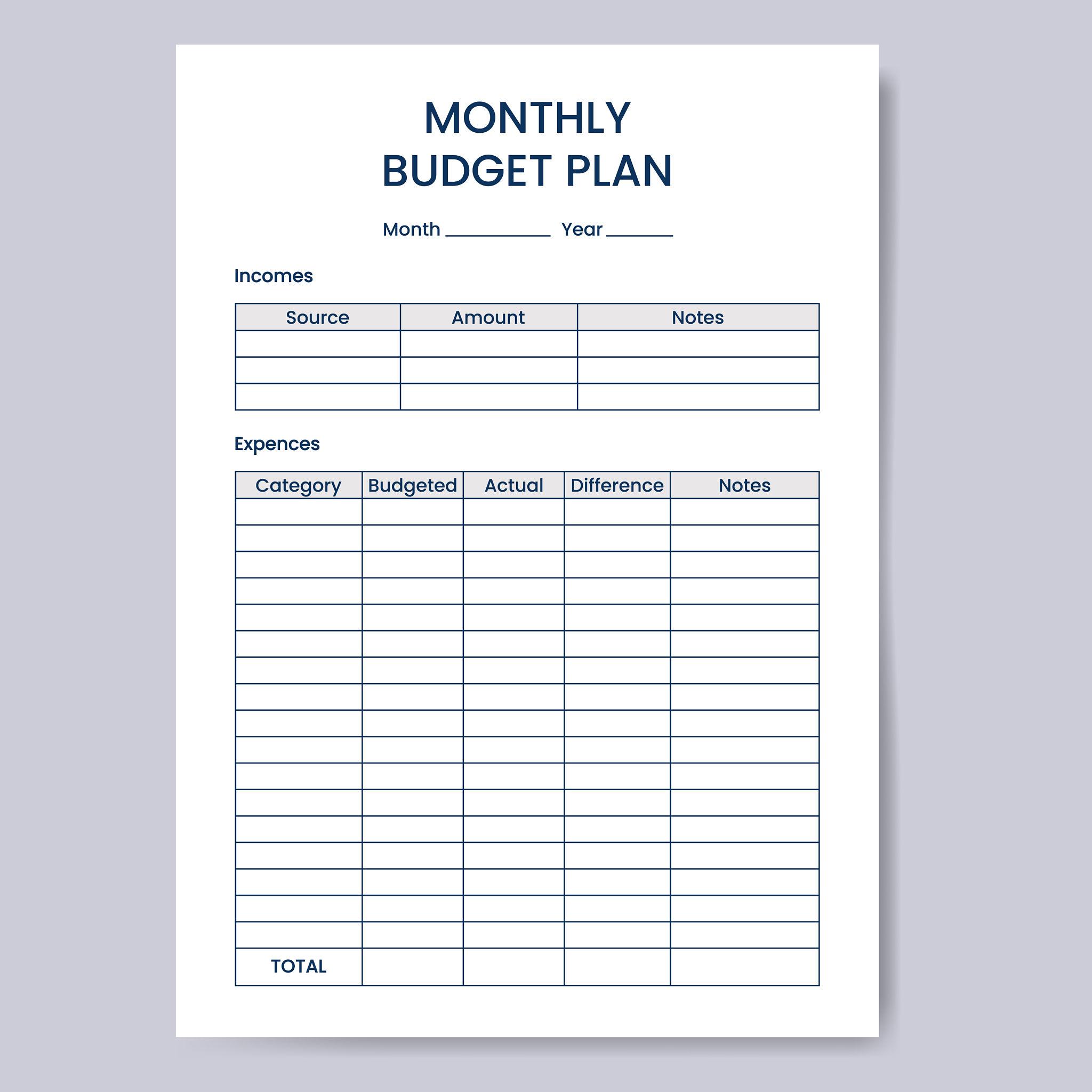

A monthly budget template makes the process much easier. Instead of building a budget from scratch, you can simply fill in your numbers and see exactly where your money is going.

In this guide, you’ll learn what a monthly budget template should include, how to use one, and how it can help you stay consistent with your financial goals.

Why a Monthly Budget Template Helps

A monthly budget template removes the guesswork from budgeting. Instead of wondering how to organize your finances, the structure is already built for you.

Using a template helps you:

- Track your income and expenses clearly

- See where your money is going each month

- Avoid overspending in certain categories

- Stay consistent with your budgeting habits

If you’re new to budgeting, starting with a template can make the process much less overwhelming.

What Should Be Included in a Budget Template

A simple monthly budget template should include the main categories most people spend money on.

Common categories include:

Income

This includes your paycheck, freelance income, side hustles, or any other money you receive.

Housing

Rent or mortgage payments, property taxes, and home maintenance.

Utilities

Electricity, water, internet, phone bills, and other household services.

Food

Groceries and dining out.

Transportation

Gas, public transportation, car payments, and insurance.

Savings

Emergency fund contributions, retirement savings, and other financial goals.

Personal Spending

Entertainment, subscriptions, shopping, and hobbies.

If you’re unsure how to organize your expenses, check out our full guide on budget categories to structure your budget properly.

Simple Monthly Budget Example

Here is a very simple example of how a monthly budget might look.

Monthly Income: $4,000

Housing: $1,400

Utilities: $250

Food: $500

Transportation: $300

Savings: $800

Personal Spending: $450

Other Expenses: $300

Total Expenses: $4,000

This type of structure helps ensure that every dollar has a purpose. Many people use systems like zero-based budgeting or the 50/30/20 rule to organize their spending.

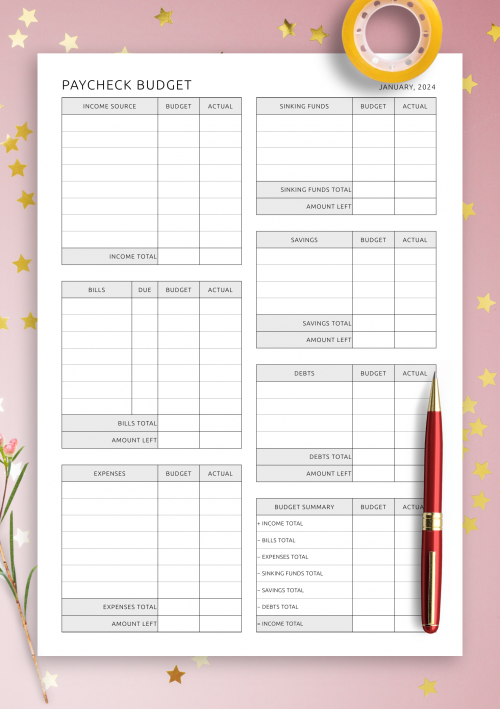

How to Use a Monthly Budget Template

Using a budget template is straightforward.

Step 1: List your total monthly income

Start by writing down the total money you expect to receive during the month.

Step 2: Add your fixed expenses

These include rent, insurance, loan payments, and subscriptions.

Step 3: Estimate variable expenses

Groceries, transportation, and entertainment may change from month to month.

Step 4: Allocate money toward savings

Set aside money for emergency savings or other financial goals.

Step 5: Review your budget regularly

At the end of the month, compare your planned spending to what you actually spent.

Tips for Sticking to Your Budget

Creating a budget is only the first step. The real challenge is staying consistent with it.

Here are a few tips to make budgeting easier:

Keep your budget simple so it’s easy to follow.

Review your spending weekly instead of waiting until the end of the month.

Adjust categories when your expenses change.

Focus on progress rather than perfection. Budgeting is a skill that improves over time.

A monthly budget template can make managing your finances much simpler. By organizing your income and expenses in one place, you can clearly see where your money is going and make better financial decisions.

If you’re just starting your budgeting journey, using a simple template is one of the easiest ways to build a consistent financial routine.

If you prefer tracking money week by week, you may also want to try using a weekly budget template to stay organized.

About the Author

Hi, I’m Akhila. I created Budgeting Made Simple to help beginners build clear, practical money systems without feeling overwhelmed.

My goal is to simplify budgeting, saving, and debt payoff into steps anyone can follow consistently. Personal finance doesn’t need to be complicated — it just needs structure and clarity.